IFRS EU endorsement process [June 2026]

The European Financial Reporting Advisory Group (EFRAG) updated its report showing the status of endorsement of each IFRS, including standards, interpretations, and amendments, most recently on 19 June 2026.

The European Sustainability Reporting Standards (ESRS) are among the key instruments designed to ensure transparent and comparable sustainability-related information from undertakings within the EU. This article provides an overview of the recently published draft revision of these standards, which promises simplification of certain requirements while at the same time introducing new demands on the quality and strategic approach to sustainability reporting. Read on to learn which changes are being proposed, what their potential impact on companies may be, and what needs to be considered in the months ahead.

The ESRS were developed on the basis of the Corporate Sustainability Reporting Directive (CSRD) and constitute the mandatory European framework requiring undertakings to disclose information on the impacts of their activities on the environment and society. The objective of these standards is to provide reliable and comparable data for investors, regulators, and the public.

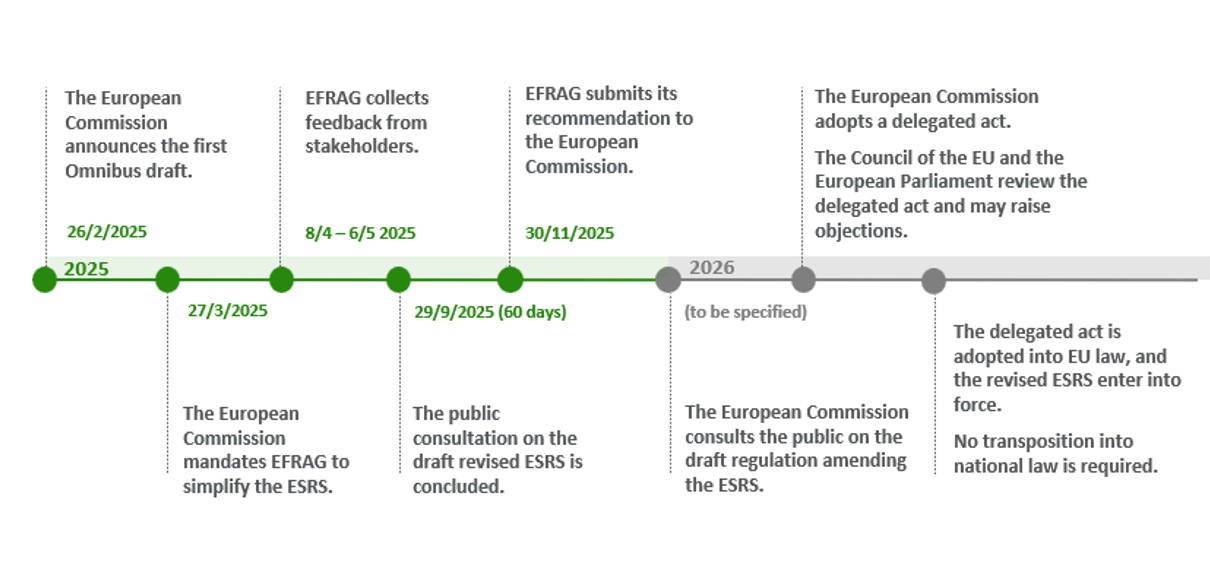

In July 2025, a draft package of substantial amendments to the ESRS was published, responding to initial experience with the application of the requirements and to calls for simplification. This proposal, building on the Omnibus package issued in February, seeks to remove duplicative and superfluous disclosure requirements and to align the European standards with global frameworks – in particular with standards of the International Sustainability Standards Board (ISSB) developed under the IFRS Foundation.

In its Consultation Paper on ESRS Revisions, published on its official website, EFRAG emphasised that the objective of the new proposal is to provide undertakings with more flexible and efficient reporting tools that better reflect actual impacts and facilitate the integration of sustainability into corporate strategy. At the same time, EFRAG stressed that simplification is not merely about reducing the number of requirements but also about a shift towards ‘materiality-based reporting’, where disclosed information must be relevant and strategically substantiated.

As highlighted in an analysis by IAS Plus, the draft focuses on enhancing the usability of the standards with an emphasis on flexibility in the assessment of materiality and on streamlining reporting, while simultaneously requiring undertakings to apply greater rigour in justifying the information disclosed and in embedding it strategically within their business models.

The public consultation on the draft is open until 29 September 2025. Subsequently, EFRAG shall submit the revised standards to the European Commission, which shall initiate the endorsement process – a stage that may result in further amendments. If the process proceeds as planned, the simplified ESRS are expected to enter into force by the end of 2026.

The proposed revision of the ESRS introduces changes that will affect how sustainability information is reported by undertakings subject to the CSRD. Companies that have already begun reporting under the current standards will need to reassess their processes in the coming months and adapt them to the new requirements once the revised standards are endorsed and enter into force.

The new framework reduces the number of mandatory datapoints and offers greater flexibility in the assessment of materiality, which may lead to more efficient data collection and a sharper focus on the most relevant aspects of sustainability. On the other hand, the revised rules place increased emphasis on transparent justification of the information disclosed and its integration with the undertaking’s business strategy.

Given the timeline for the adoption of the revised standards, undertakings are advised to monitor further developments, make use of the public consultation period to assess potential impacts, and prepare for possible changes in their reporting methodologies. This approach may support a smoother transition to the new requirements and minimise potential operational or cost-related impacts.

Seminars, webcasts, business breakfasts and other events organized by Deloitte.