IFRS EU endorsement process [June 2026]

The European Financial Reporting Advisory Group (EFRAG) updated its report showing the status of endorsement of each IFRS, including standards, interpretations, and amendments, most recently on 19 June 2026.

The extensive amendment to Act No. 563/1991 Coll., on Accounting, as amended (the “Accounting Act”), has introduced “categorisation of reporting entities”, effective since 1 January 2016. A more detailed classification should allow for more appropriate adjustment of obligations in the reporting and presentation of accounting information

Micro entities continue to be “protected” by the EU Directive and Member States are not allowed to increase the entities’ administrative obligations. On the contrary, this does not apply to large entities from which a Member State may require, in justified cases, more information, more extensive reporting etc. Legislation defines minimum requirements for information to be disclosed in notes to the financial statements for various categories; however, it is at an entity’s discretion to disclose more information than the required minimum. Categorisation also relates to the statutory audit of financial statements.

Since 1 January 2016, new criteria have been applied to categorise reporting entities, whereby two criteria out of three have to be met in order to classify an entity within a category.

Two years after the implementation of the Act, it has become relatively clear that the legislator required assets to be assessed using their net values. Let me just remind you that the definition of turnover is hidden at the very end of Appendices 2 and 3 to Regulation No. 500/2002 Coll., providing implementation guidance on certain provisions of the Accounting Act, as amended, for entities that are businesses maintaining double-entry accounting records (“Regulation”). The turnover is defined as the sum of Sales of goods + Sales of services + Other operating income + Income from non-current financial assets + Income from other non-current financial assets + Interest income + Other financial income. In practice, however, we are often asked how to classify a specific reporting entity appropriately and when to change its category.

Section 1e of the Act stipulates that if a reporting entity exceeds or ceases to exceed two limit values under Sections 1b and 1c as of two subsequent balance sheet days of regular financial statements the reporting entity changes the category under which the scope and method of preparation of the financial statements is defined starting from the beginning of the immediately following reporting period.

The frequent source of incorrect classification or a premature change of the reporting entity’s category is the inconspicuous interim provision of the Act stipulating how reporting entities are arranged on the starting line after the adoption of the amended Act and from which date the reporting periods are counted.

In the reporting period started in 2016, a reporting entity follows the legal regulations for a category of reporting entities and a category of groups of reporting entities the conditions of which were met as of the balance sheet date immediately preceding the reporting period.

This means that in the first year of the amendment application (ie in 2016), the requirements as of 31 December 2015 were applied and the reporting entity was categorised accordingly. The first classification is not included in the calculation of the “number of limit value excesses”.

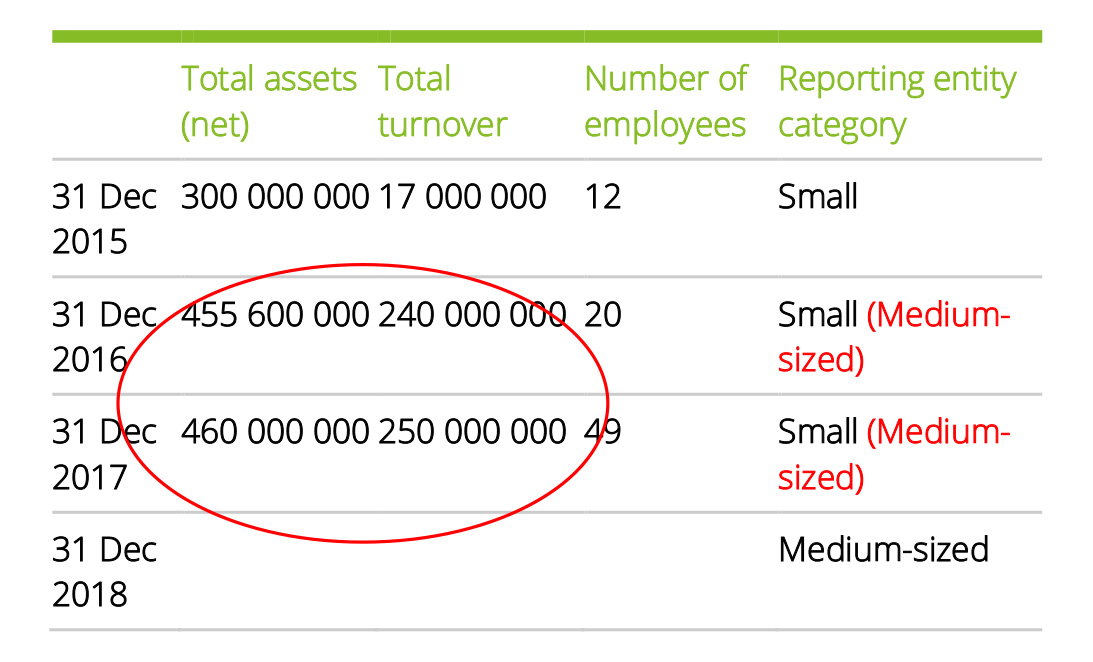

At the start (as of 1 January 2016), the reporting entity is classified as a “small” entity according to the results as of 31 December 2015. This first classification is not included in the number of periods in which the excess of limit values is monitored.

Even though the entity was doing well in the following two years and exceeded two limit values (assets and turnover) to be reclassified as “medium-sized” as of two subsequent balance sheet days, it continues to report as a small entity in 2016 and 2017. Only after exceeding two out of the three limit values in two subsequent years it starts reporting under another category, in our example as a medium-sized entity.

This consideration is not complex and most people reading the Act carefully enough will have no problem to apply it correctly. Let us give you a more complicated example.

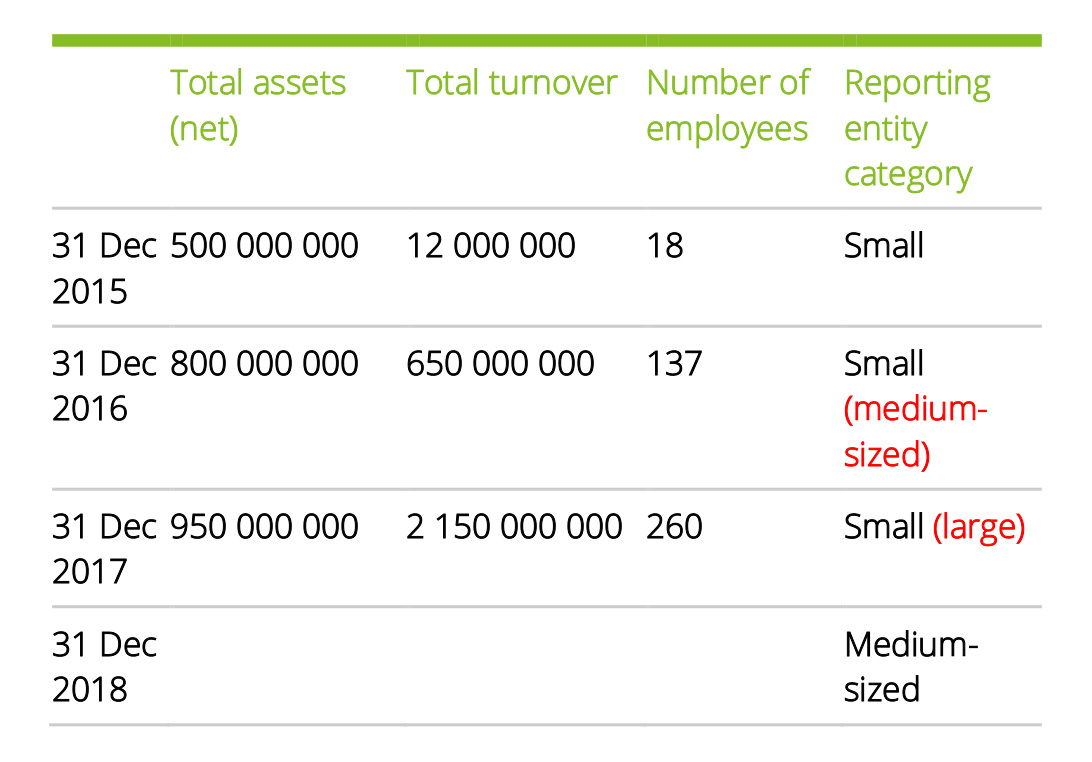

In this example, the reporting entity has grown rapidly. At the start, it was classified as “small” according to its results in 2015 and continued to report as “small” in 2016 and 2017. As of the first tested balance sheet date on 31 December 2016, it exceeded two out of the three categories to become a “medium-sized” entity. As of the second balance sheet date on 31 December 2017, it even achieved the values attributable to the “large” category.

It is obvious in this case that the reporting entity has to change its category in 2018; the question may be what classification is appropriate – is it a medium-sized or a large entity? The reporting entity exceeded two limit values for the “medium-sized” category as of two subsequent balance sheet dates of regular financial statements and the values for the “large” category as of the latter balance sheet date.

In applying Section 1e of the Act, we have to come to the conclusion that the reporting entity exceeded limit values for the “medium-sized” category as of two balance sheet dates (for the “large” category only once) and thus in the 2018 reporting period it will report as a “medium-sized” entity.

In conclusion, there is the most interesting example:

Example 3

A small entity merges by amalgamation with a large entity. The small entity is the successor. If we strictly applied the letter of the law we would come to the following conclusion:

- No establishment or start of activities under Section 1e occurred, ie the category of the reporting entity is not estimated and the original category of a “small” entity continues to apply.

- Two limit values were not exceeded under Sections 1b and 1c as of two subsequent balance sheet dates of regular financial statements, ie the category of the reporting entity will not be changed for two years.

The large entity that merged by amalgamation with the small entity thus becomes small with all of the advantages for financial statements presentation and other reporting.

We believe that such treatment would violate the correctness principle that prevents avoiding the purpose of the law. Section 8 (2) of the Act stipulates that accounting books are considered correct if maintained by the reporting entity in compliance with and without avoiding the purpose of the Act and other legal regulations. It is contrary to this principle if in fact a large entity takes advantages of small entity reporting through a formal transaction.

As stated at the beginning, the purpose of reporting entity categorisation is to determine the corresponding related obligations contained in other sections of the Act, or legal regulations directly relating to accounting, such as the Act on Auditors. Meeting relevant obligations is assumed by law starting from the establishment of an entity, or from the date on which the entity starts its activities. If the obligations are applicable to newly established entities or entities starting their activities the more they apply to entities that undergo transformations.

Although there is no doubt that the approach to similar transactions will be adjusted in practice over time we recommend changing the category in similar situations depending on the evidence available after the transformation in the financial statements for previous periods, taking into account the “substance over form” principle and in our example, we would change the category to “large”.

Seminars, webcasts, business breakfasts and other events organized by Deloitte.