IFRS EU endorsement process [June 2026]

The European Financial Reporting Advisory Group (EFRAG) updated its report showing the status of endorsement of each IFRS, including standards, interpretations, and amendments, most recently on 19 June 2026.

IFRS 15 Revenue from Contracts with Customers became effective on 1 January 2018. As the new standard introduces significant changes in revenue recognition in comparison to the existing regulation, we would like to resume our series of articles focusing on IFRS 15 in greater detail.

Our Accounting News of May 2017 discussed the issues relating to the sequence of revenue steps and the application of the portfolio approach. In September 2017, the Accounting News elaborated on the requirements of IFRS 15 relating to the identification of contracts with customers. By way of reminder, please note that detailed articles focusing on IFRS 15 were published in the Accounting News of July 2014, October 2014 and December 2016.

Transition to the new standard

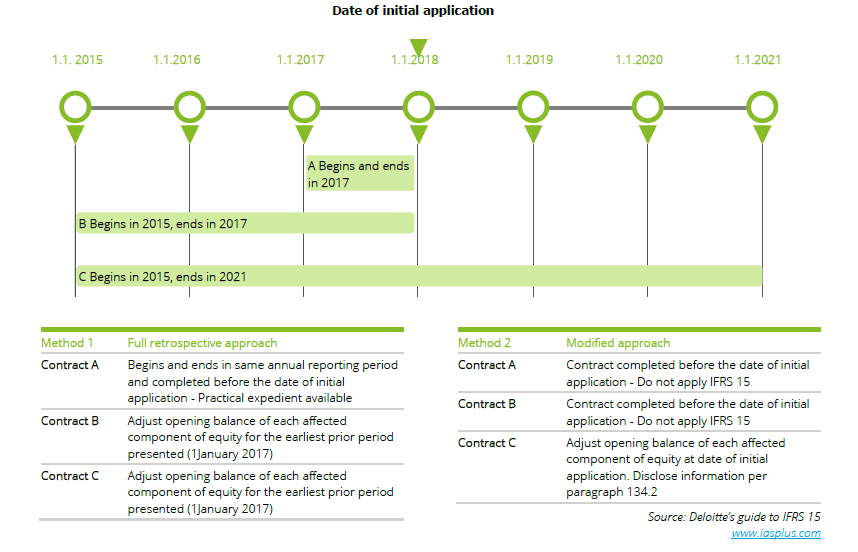

Appendix C of IFRS 15 provides detailed guidance for entities transitioning to the Standard for the first time. Entities have two options in transitioning to IFRS 15 – a full retrospective approach and a modified approach. Both options are fairly detailed but helpful in providing some relief on the initial application of IFRS 15.

For the purposes of the transition provisions, the date of initial application is the start of the reporting period in which an entity first applies IFRS 15. For example, the date of initial application in respect of entities applying IFRS 15 for the first time in the financial statements for the year ending 31 December 2018 will be 1 January 2018.

Method 1 – Full retrospective approach

Entities can apply IFRS 15 retrospectively to each prior reporting period presented in accordance with IAS 8 Accounting policies, Changes in Accounting Estimates and Errors. Under this option, prior year comparatives are restated, with a resulting adjustment to the opening balance of equity in the earliest comparative period.

IFRS 15 provides the following optional practical expedients:

1. For completed contracts (i.e. contracts for which the entity has transferred all of the goods or services identified in accordance with IAS 11 Construction Contracts, IAS 18 Revenue and related Interpretations), entities are not required to restate contracts that begin and end within the same annual reporting period. For example, entities first applying IFRS 15 as of the 31 December 2018 year end will not need to restate contracts entered into and completed in 2017.

2. For completed contracts, entities are not required to restate contracts that were completed at the beginning of the earliest period presented. For example, for an entity first applying IFRS 15 for a 31 December 2018 year end and presenting comparative information for the year ended 31 December 2017 only, contracts completed by 31 December 2016 do not need to be evaluated.

3. For completed contracts that have variable consideration, an entity may use the transaction price at the date the contract was completed rather than estimating variable consideration amounts in the comparative reporting periods. This means, in particular, that if the consideration had ceased to be variable by the time the contract was completed (which is the case for many, but not all, contracts), the transaction price can be based on the amount that was ultimately payable by the customer. For example, for contracts completed prior to 31 December 2017, entities first applying IFRS 15 as of the 31 December 2018 year end may base earlier revenue figures on the consideration (including any variable consideration) that was ultimately payable (or at least the estimate of the variable consideration as of the date on which the contract was completed) rather than estimate the variable consideration at earlier dates.

4. For contracts that were modified before the beginning of the earliest period presented, an entity is not required to apply the requirements for contract modifications separately to each earlier modification. Instead, an entity shall reflect the aggregate effect of those modifications when

- Identifying the satisfied and unsatisfied performance obligations;

- Determining the transaction price; and

- Allocating the transaction price to the satisfied and unsatisfied performance obligations.For example, entities first applying IFRS 15 as of the 31 December 2018 year end and presenting comparative information for the year ended 31 December 2017 only, will, in respect of each of the requirements listed above, account for a contract that was modified one or more times before 1 January 2017 as though all modifications had been part of the contract as originally agreed. Please note that any modifications after 1 January 2017 would need to be accounted for individually.

5. For all reporting periods presented before the date of initial application, an entity need not disclose the amount of the transaction price allocated to the remaining performance obligations and an explanation of when the entity expects to recognise that amount as revenue. For example, entities first applying IFRS 15 as of the 31 December 2018 year end will not be required to make any disclosures about the performance obligations remaining as of 31 December 2017 in respect of contracts yet to be completed as of that date.

If used, the practical expedients should be applied consistently to all prior periods presented and disclosure should be made as to which expedients have been used. To the extent reasonably possible, a qualitative assessment of the estimated effect of applying each of those expedients should be provided.

Method 2 – Modified approach

Under the modified approach, entities can apply IFRS 15 only from the date of initial application. If they opt to do so, they will need to adjust the opening balance of retained earnings (or another component of equity, as appropriate) at the date of initial application (i.e. 1 January 2018), but they are not required to adjust prior year comparatives. This means that they do not need to consider contracts that had been completed prior to the date of initial application. In broad terms, the figures for comparative periods will remain on the previous basis. When using this approach, entities can elect to apply IFRS 15 retrospectively only to contracts that are not completed contracts at the date of initial application.

Additionally, entities applying the modified approach may use the practical expedient in respect of contract modifications that is available for entities applying the full retrospective approach either for:

If the modified approach is used, entities must disclose the amount by which each financial statement line item is affected in the current reporting period as a result of applying IFRS 15, including an explanation of the reasons for the significant changes between the results reported under IFRS 15 and the previous revenue guidance followed.

The erticle is part od dReport – September 2018, Accounting news.

Seminars, webcasts, business breakfasts and other events organized by Deloitte.