IFRS EU endorsement process [June 2026]

The European Financial Reporting Advisory Group (EFRAG) updated its report showing the status of endorsement of each IFRS, including standards, interpretations, and amendments, most recently on 19 June 2026.

There has been an evolution in the technological architecture of entities across the world. This has resulted in potentially significant accounting changes for entities that have entered into cloud-computing arrangements. The IFRS Interpretations Committee has published two agenda decisions clarifying how arrangements in respect of a specific part of cloud technology, Software-as-a-Service (SaaS), should be accounted for.

The IFRS Interpretations Committee agenda decisions may have a significant impact on many entities, in both the private and public sectors, irrespective of size and industry.

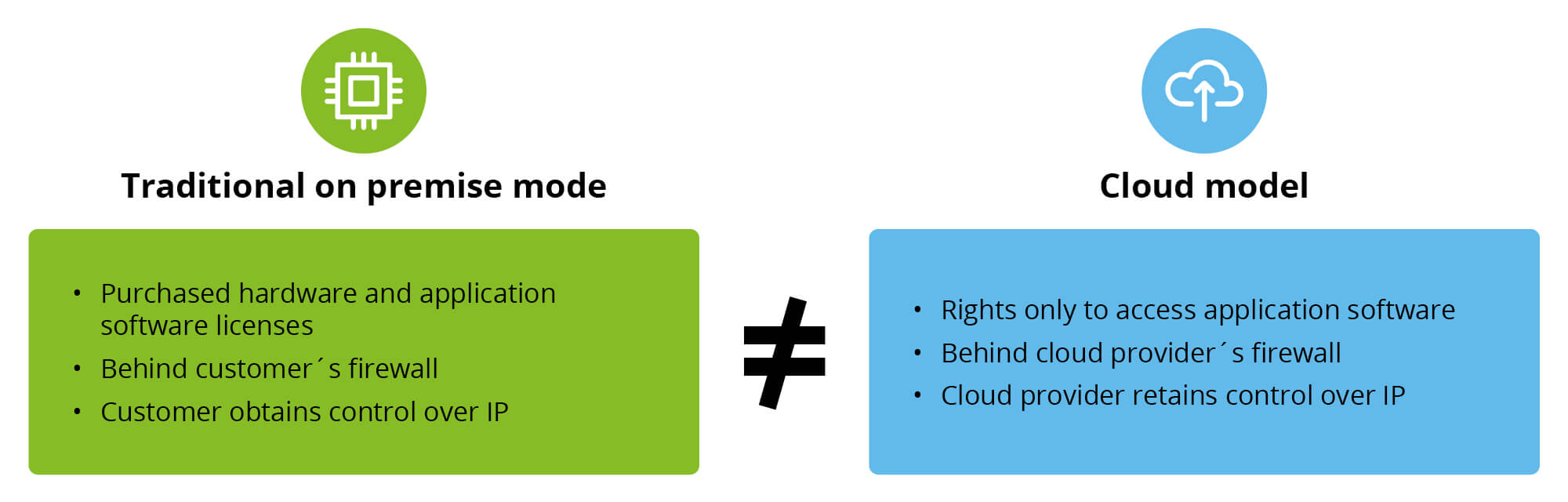

To understand the conclusions reached by the IFRS Interpretations Committee, it is helpful to understand the main differences between the traditional on-premise and cloud-based technology models. Although the front-end appearance is broadly consistent, there are significant differences, as highlighted in the diagram, which result in the different accounting conclusions.

SaaS arrangement – service or asset?

The IFRS Interpretations Committee in its first agenda decision, published in March 2019, addressed the customer’s accounting for a Software-as-a-Service (SaaS) arrangement where the customer pays a fee in exchange for a right to receive access to the supplier’s application software for a specified term. The IFRS Interpretations Committee concluded that SaaS arrangements are likely to be service contracts, rather than intangible or leased assets. This is because the customer typically only has a right to receive future access to the supplier’s software running on the supplier’s cloud infrastructure and therefore the supplier controls the intellectual property of the underlying software code.

Nevertheless, in certain SaaS arrangements, the customer may obtain an intangible asset. This may be the case when:

- The customer has the contractual right to take possession of the software during the hosting period without significant penalty.

- It is feasible for the customer to run the software on its own hardware or contract with a party unrelated to the supplier to host the software.

Accounting for configuration and customisation services in implementing SaaS arrangements

In its agenda decision published in April 2021 (the second agenda decision), the IFRS Interpretations Committee considered how an entity should account for configuration and customisation costs incurred in implementing these SaaS service arrangements and concluded:

This conclusion could result in a reduction in profit in a particular year, impacting measures such as earnings before interest and tax (EBIT), earnings before interest, tax, depreciation and amortisation (EBITDA) and profit before tax (PBT).

This represents a significant difference with the requirement applicable under US GAAP.

Where a change in accounting policy is required to apply the conclusions reached by the IFRS Interpretations Committee, an entity must account for the change applying IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors. For example, an entity may be required to derecognise costs previously recognised as an intangible asset and restate the comparative period(s).

When to implement the agenda decisions

Implementing the IFRS Interpretations Committee agenda decisions may have a significant impact on an entity’s financial statements. Unlike new or amendments to existing IFRS Standards which have a specific future application date, IFRS Interpretations Committee agenda decisions have no effective date. However, the Due Process Handbook of the IFRS Foundation explains that it would be expected that an entity would be entitled to sufficient time to make that determination and implement any necessary accounting policy change. Determining how much time is sufficient to make an accounting policy change is a matter of judgement that depends on an entity’s particular facts and circumstances.

Nonetheless, an entity would be expected to implement any change on a timely basis and, if material, consider whether disclosure related to the change is required by IFRS Standards.

More information

You can find detailed discussion on these agenda decisions including practical implications for financial reporting (e.g. change in accounting policies and illustrative note disclosures) and wider business impacts in Deloitte publication issued in June 2021:

A Closer Look — Software-as-a-Service arrangements — Accounting changes are the result of an era of digital transformation

Sources: www.iasplus.com, A Closer Look from June 2021

Seminars, webcasts, business breakfasts and other events organized by Deloitte.