Since 1 January 2023, the minimum wage has increased to CZK 17,300. This has led to changes in the amounts of taxes and contributions for selected groups of employees. The rates of foreign and domestic meal allowances and rates of reimbursement of travel expenses have also been adjusted. Furthermore, the threshold for applying progressive income tax has changed and the basic non-distrainable amount has increased. These are just some of the changes that will affect the payroll environment in 2023. You can read an overview of all the major changes in our article.

Maximum assessment base for social security contributions in 2023

The maximum assessment base for social security contributions has increased from CZK 1,867,728 to CZK 1,935,552 in 2023.

Increase in minimum wage from 1 January 2023

Since 1 January 2023, the minimum wage has increased by CZK 1,100 to CZK 17,300; the minimum hourly wage has increased to CZK 103.80. The bottom levels of guaranteed wages for individual work groups have also been increased to CZK 17,300 – CZK 34,600 (8 groups depending on complexity, responsibility a strenuousness of the work performed). The increase in the minimum wage has an effect, for example, on the limit establishing entitlement to a tax bonus (the annual income amounts to at least six times the minimum wage / at least half of the minimum wage per month, i.e. CZK 8,650); the maximum amount of earnings of a job seeker registered by the Labour Office (half of the minimum wage); the amount of state social support allowances except for allowances reflecting the applicant’s income; increase in the maximum tax relief for the placement of a child in a pre-school facility (in the amount of the minimum wage); increase in the limit to exempt pensions from income tax (up to a 36 multiple of the minimum wage, i.e. CZK 622,800 for 2023).

New amount of the minimum assessment base for health insurance in 2023

With respect to the change in the minimum wage since January 2023, there has been an increase in the minimum assessment base for health insurance and thus the minimum amount of the monthly premium to be paid by individuals with no taxable income that is paid on behalf of, for example, the so-called state categories of the insured (students, old age pensioners, women on maternity leave, recipients of parental allowances, job seekers registered by the Labour Office, etc.). In 2023, the minimum monthly assessment base for health insurance is CZK 17,300 and the monthly premium is CZK 2,336.

Change in the basic rates of meal allowances for trips abroad for 2023

Since 1 January 2023, some foreign meal allowances have been subject to changes. The countries affected by the changes are: Poland (EUR 45), Finland (EUR 55), Sweden and Denmark (EUR 60). There will also be changes for non-European countries, e.g. Brazil (USD 60), Australia (USD 65), Morocco and Egypt (EUR 45).

Reimbursement of business trip expenses and local meal allowance rates for 2023

Since 1 January 2023, adjustments have been made to the rates of reimbursement of travel expenses paid to employees on business trips. In connection with the use of a private car for a business trip, employees are entitled to the compensation for car wear as well as compensation for consumed fuel. The compensation for car wear has been increased to CZK 5.20 per km driven in 2023. If employees claim compensation for consumed fuel using the prices published in a regulation, they may request compensation of CZK 41.20 per 1 litre of consumed Natural 95, CZK 45.20 per 1 litre of consumed Natural 98, CZK 44.10 per 1 litre of consumed diesel oil and CZK 6 per 1 kilowatt hour of consumed electricity. Instead of prices determined by a regulation, employees are naturally entitled to claim compensation based on their actual expenses determined using confirmations of fuel payment.

In 2023, local meal allowance rates will be increased in individual time zones. Newly, employees are entitled to meal allowance of at least CZK 129 if their business trip takes from 5 to 12 hours; CZK 196 if their business trip takes more than 12 hours but less than 18 hours; and CZK 307 if their business trip exceeds 18 hours. The principle of meal allowance reduction remains the same.

Monetary meal allowance

The meal-voucher flat rate (monetary meal allowance) is exempt from income tax on the employee’s side only up to a specified limit, namely 70% of the upper limit of the meal allowance that can be granted to salaried employees during a business trip lasting 5 to 12 hours. For 2023, the monetary meal allowance will thus be tax-exempt up to CZK 107.10 per shift. If an employer provides a higher monetary meal allowance to an employee, the difference must be taxed in the employee’s salary and social security and health insurance contributions must be paid on the difference.

Average gross wage for Q1–Q3 2022

On 5 December 2022, the Czech Statistical Office published the average wage for a period between the first and the third quarters of 2022 in the amount of CZK 39,306 (the previous amount was CZK 37,047). This amount is used to calculate values for meeting the obligatory proportion of disabled individuals in 2022. In order to compensate one disabled person with a “substitute performance”, products and services of CZK 275,142 excluding VAT need to be consumed (7 times the average wage, i.e. 39,306 x 7). Contribution to the state budget relating to one vacant full-time position that should have been staffed with a disabled person would be CZK 98,265 (2.5 times the average wage, i.e. 39,306 x 2.5).

The maximum amount of salary compensation for camp leaders is therefore also CZK 39,306 for 2023.

Amount of tax relief for child placement (pre-school allowance)

The minimum wage amount has an effect on the maximum amount of tax relief for a child placed in a pre-school facility, i.e. the pre-school allowance. The relief equals the minimum wage. This means that while in 2022 parents having a child in a kindergarten might utilise a tax relief of up to CZK 16,200, this year the amount is CZK 17,300.

The threshold for applying progressive income tax

Since 2021, the income of individuals has been taxed at a 15% tax rate up to the threshold of the tax base of 48 times the average wage (i.e. in 2023 up to CZK 161,296 per month, CZK 1,935,552 per year). The annual tax base over 48 times the average wage is taxed at a higher rate of 23%.

Increase in the decisive income for participation in the sickness insurance scheme and increase in withholding tax

Since 1 January 2023, the threshold for employee participation in the sickness insurance scheme has increased from CZK 3,500 to CZK 4,000. The limit for the application of withholding tax on income from an agreement to perform work or employment agreement, unless the employee has made a taxpayer’s declaration, is also linked to the aforementioned decisive income – thus the amount of CZK 4,000 is applicable in 2023. In case of agreements to complete a job, the limit of recognised income of up to CZK 10,000 still applies.

Social security contribution discount

With effect from 1 February 2023, companies will be able to claim a 5% discount on social security for selected groups of employees if certain conditions are met. This will reduce the contribution from the original 24.8% to 19.8%. The discount thus may be applied to wages for February for the first time, provided that the stipulated conditions are met for the whole month.

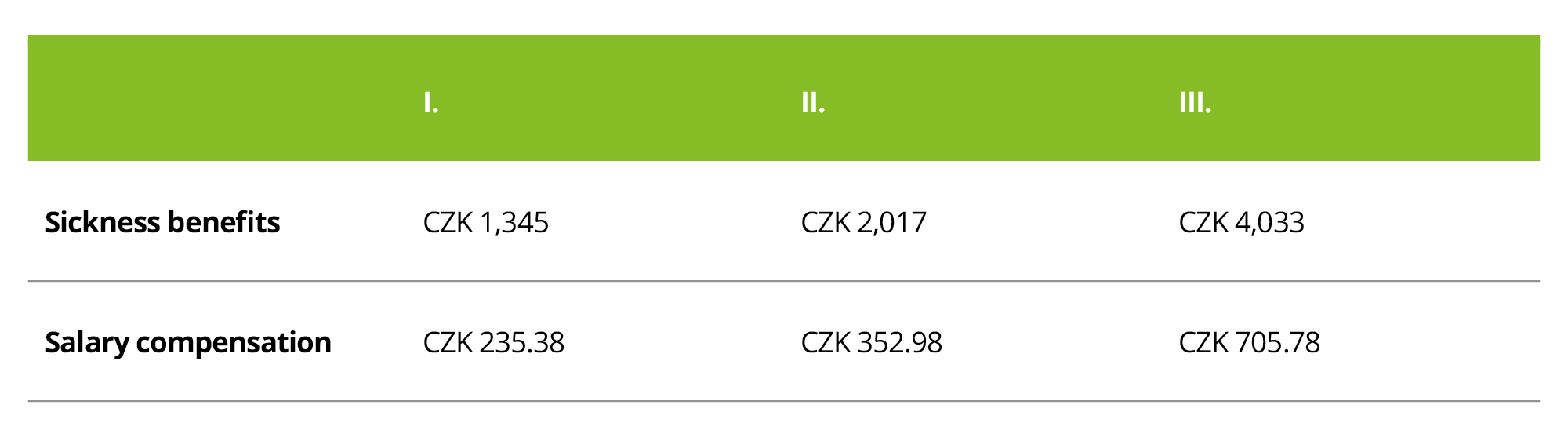

Change in reduction limits

Since 1 January 2023, the reduction limits for the calculation of salary compensation and sickness benefits have been changed and are presented in the table below:

Expansion in the provision of postnatal paternity leave

Since 1 December 2022, the postnatal paternity leave benefit has been extended to include cases related to the stillbirth or death of a child. A father will be entitled to paternity leave on account of the death of a child even if the father of that child has already drawn paternity leave on account of caring for that child (this also applies to cases when one of the children born at the same time dies). The entitlement to paternity leave in the case of a stillbirth or a child who dies within 6 weeks of the date of birth will arise provided that the event occurs on 1 December 2022 at the earliest.

Increase in premium rates for paramedics and professional firefighters

Since 1 January 2023, the rate of employer-paid pension insurance scheme premiums for professions that will have the option of early retirement (paramedics, professional firefighters, etc.) has increased. This rate will continue to increase over the next 3 years and will be reported on a separate line on the insurance premium statement. The rate will increase by 5% and the increase will be phased as follows:

- In the first year, it will increase by 2%, i.e. 26.8% of the assessment base.

- In the second year, it will increase by 3%, i.e. 27.8% of the assessment base.

- In the third year, it will increase by 4%, i.e. 28.8% of the assessment base.

- In the fourth year, it will increase by 5%, i.e. 29.8% of the assessment base.

Increase in non-distrainable amount from January 2023

Since 1 January 2023, the basic non-distrainable amount for the calculation of enforcement, insolvency, statutory and agreed deductions has been increased to CZK 13,638, based on an increase in the subsistence level income to CZK 4,860 and an increase in the normative cost for housing to CZK 15,597. For each dependant, the obligor’s non-distrainable amount will be newly increased by CZK 3,409.5. The amount has decreased by CZK 291.75 compared to the previous amount due to a change in the calculation. The new amount is ¼ of the non-distrainable amount, previously it was ⅓. The limit above which the obligor’s wages can be deducted without restrictions will be CZK 30,685.5.

New limit for applying “kurzarbeit”

In the event that the “allowance in a period of partial unemployment” is applied in 2023, the limit up to which the state allowance can be drawn will be updated in connection with the new average wage for Q1–Q3 of 2022. This involves reimbursement of 80% of the compensation paid for obstacles at work, including the insurance premiums paid by the employer, up to a maximum of 1.5 times the average wage (CZK 39,306), i.e. up to CZK 58,959.

Change in the sample form for annual account of prepayments for 2022

On 13 December 2022, the General Financial Directorate published a new sample form for the Request for Annual Account of Prepayments and Tax Benefits – form 25 5457/B – sample no. 3. Sample no. 3 is intended for taxpayers who apply for the annual account of prepayments and tax benefits for tax period 2022 and who claim tax relief for ceased enforcement proceedings with the taxable entity. Older versions of the sample form can be used provided that taxpayers do not want to claim tax relief for ceased enforcement proceedings; taxpayers who do not want to utilise interest on a loan for financing housing should use sample no. 1, which is still in the tax form database.

At the same time, a new sample form has been published – form 25 5460/1, sample no. 27, Calculation of Tax and Tax Benefits for the 2022 Tax Year – which includes the abovementioned tax relief for ceased enforcement proceedings.

Amendment to the Decree regulating occupational healthcare services

On 1 January 2023, Decree No. 452/2022 Coll., on specific healthcare services, came into force. Although the possibility of abolishing initial occupational health examinations for selected groups of employees was discussed during the autumn of 2022, the Decree still imposes the obligation to carry out initial occupational health examinations. Changes were eventually made, in particular, with regard to periodic examinations, which are no longer compulsory in the first and second categories of employees and are to be carried out only if the employee or the employer so requires. However, periodic examinations are still compulsory for the third and fourth categories and the second risk category of employees.

The Decree also provides for changes to the procedures for requesting such examinations and to the content of the examinations.